What Is a Fixed Deposit (FD)?

A Fixed Deposit (FD) is a financial product offered by banks, non-banking finance companies (NBFCs), and housing finance companies in India that lets you deposit a lump sum for a fixed tenure at a guaranteed interest rate. It is one of India’s most popular safe investment options because the principal and interest are assured (especially up to ₹5 lakh under DICGC insurance).

- Key benefits:

- Guaranteed returns

- Easy to open & manage

- Offers higher interest than regular savings accounts

- Special higher rates for senior citizens (usually +0.25% to +0.75%)

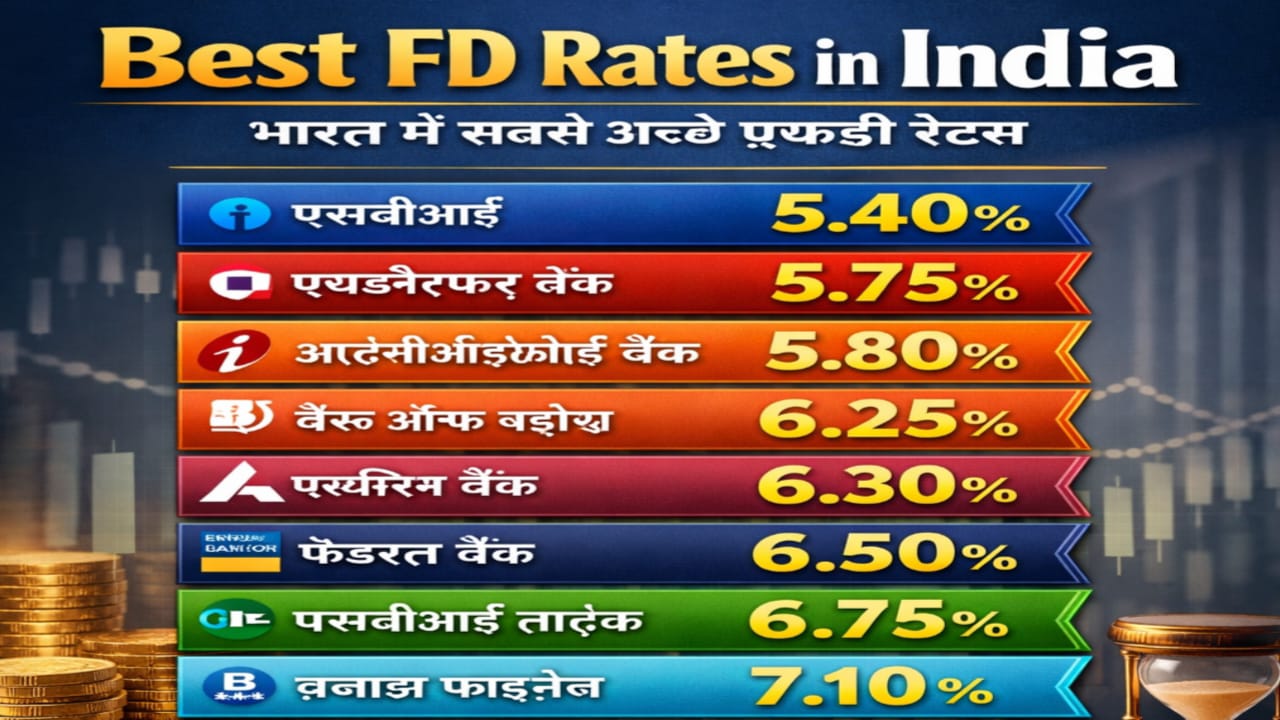

Current Best FD Rates

The Reserve Bank of India (RBI) eased monetary policy in 2025, leading many banks to adjust FD rates downward. However, several banks — especially small finance banks and NBFCs — still offer attractive interest rates.

Highest FD Rates Available

| Institution | Max Rate (General Public) | Max Rate (Senior Citizens) |

| Manipal Housing Finance (NBFC) | 8.25% | 8.25% |

| Bandhan Bank | 8.05% | 8.55% |

| Suryoday Small Finance Bank | 8.05% | 8.10% |

| Jana Small Finance Bank | 8.00% | 8.00% |

| Utkarsh Small Finance Bank | 7.65% | 8.15% |

| Shriram Finance (NBFC) | 7.60% | Higher with bonus |

| Ujjivan Small Finance Bank | 7.45% | 7.95% |

Note: Some NBFCs (non-bank lenders) also advertise very high FD yields (even above 8.5%), but risk and insurance cover may differ compared with bank FDs. Always check safety ratings and DICGC protection.

Public Sector & Major Private Banks FD Rates

For national and large private banks, rates are generally moderate but stable, backed by strong safety and wide branch networks:

| Bank | General FD Rates | Senior Citizen Rates |

| State Bank of India (SBI) | 3.05% – 6.60% | 3.55% – 7.10% |

| HDFC Bank / ICICI Bank / Axis Bank | 2.75% – 6.60% | 3.25% – 7.35% |

| YES Bank / RBL Bank / IDFC FIRST | 3.00% – 7.00% | 3.75% – 7.75% |

| Public Sector Banks (BoB, PNB, Indian Bank) | 3.00% – 6.75% | 3.50% – 7.30% |

Senior Citizens – Extra Benefit

Most banks add a special interest rate premium for senior citizens (typically between 0.25–0.75% extra). For example:

- Senior rate up to ~8.55% at Bandhan Bank’s short-term FD, higher than the general public rate.

- Many small finance banks offer senior boosts on top of competitive base rates.

How to Choose the Best FD for You

Here’s how to decide based on your goals:

1. Return vs Safety

- NBFCs & smaller banks may have higher rates, but check credit rating & DICGC protection.

- Public sector and large private banks offer stable and widely trusted safety.

2. Tenure Matters

- Short-term FDs (1–2 years): Good for liquidity and emergency planning.

- Medium/Long-term (3–5+ years): Often higher interest (especially at small finance banks).

3. Tax Implications

- Interest earned on FDs above ₹40,000 (general) and ₹50,000 (senior citizens) is taxable.

- TDS (Tax Deducted at Source) may apply.

4. Compound or Cumulative

- Cumulative FDs: Interest compounds and pays at maturity — ideal for wealth building.

- Non-cumulative: Monthly/quarterly interest payouts — useful for regular income.

Conclusion

Even in a falling interest rate environment, FDs remain an important conservative investment for many Indians — especially retirees and risk-averse savers. By comparing current rates across banks & institutions, you can align your strategy with your financial goals.