ONGC Kya Hai?

Oil and Natural Gas Corporation (ONGC) India ki Largest Oil & Gas Exploration Company Hai aur Maharatna PSU Status Rakhti Hai.

- India ka 70% Crude Oil aur 84% Natural Gas Production ONGC Karta Hai

- Established: 1956

- Parent: Government of India

- Global Presence via ONGC Videsh

India ka Energy Backbone=ONGC

Business Model (ONGC Paisa Kaise Kamata Hai?)

ONGC ka Business Mainly Upstream Sector me Hai:

Revenue Sources:

- Crude Oil Production

- Natural Gas Production

- International Assets (ONGC Videsh)

- Subsidiaries (HPCL, Petrochemicals)

Jab Crude Oil Price Badhta Hai ONGC ka Profit Generally Badhta Hai

Fundamental Analysis

Strength:

- Strong Asset Base (Oil Fields, Reserves)

- Government Backing

- High Dividend Yield

Weakness:

- Profit Oil Prices pe Dependent

- PSU Discount (Valuation Low Rehta Hai)

Example:

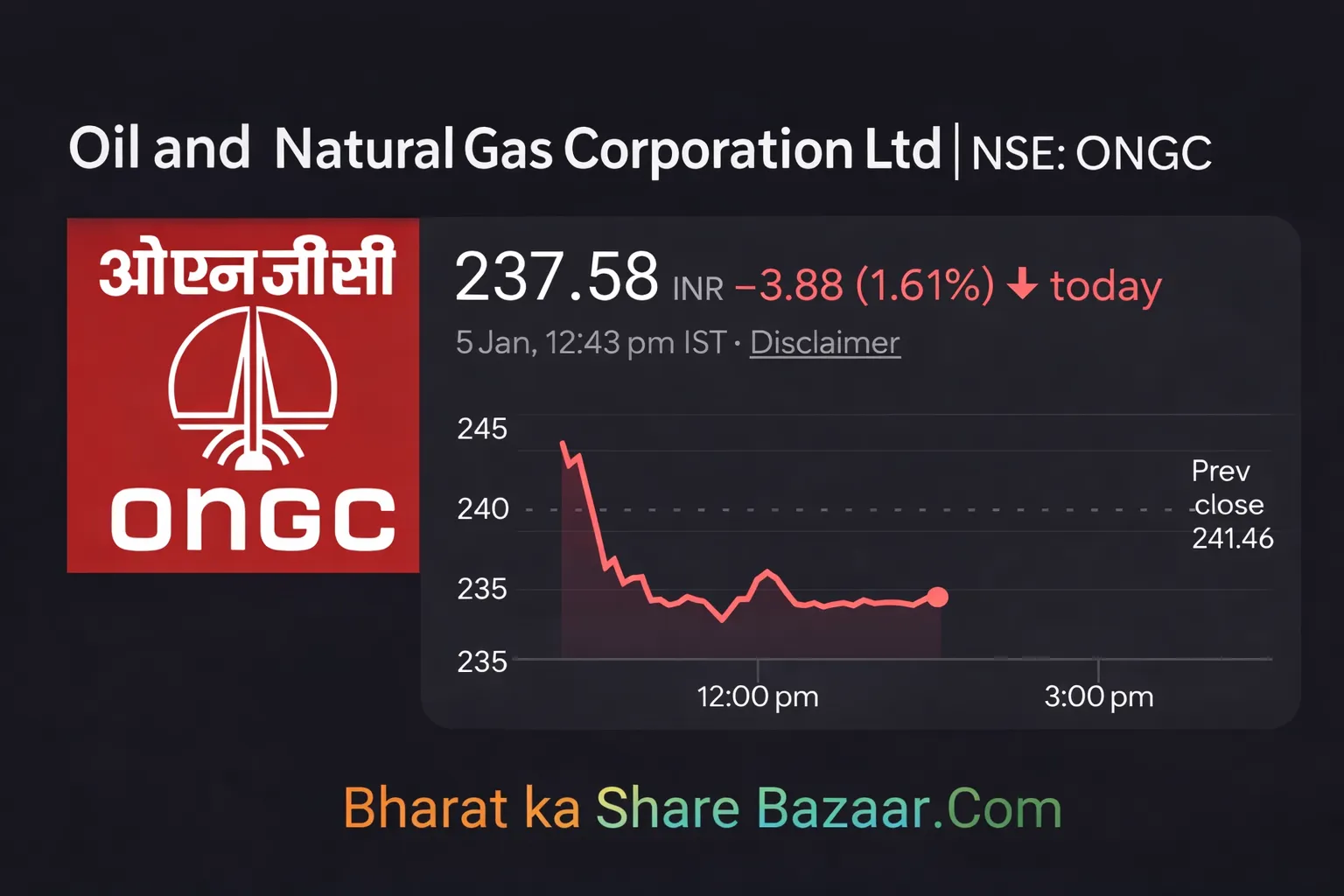

- Stock Around ₹240 – ₹270 Range me Trade Karta Raha Recently

- P/E Ratio Low (Value Stock Signal)

Growth Drivers

1. Rising Energy Demand

India ki Economy Grow ho Rahi Hai Oil Demand Increase

2. Global Oil Prices

Geopolitical Tension (Middle East) Oil Prices ko Push Karta Hai ONGC Profit Boost

3. Production Increase

- Mumbai High Output Boost (BP Partnership)

- Long Term Revenue Growth Potential

4. Renewable Expansion

ONGC Target: 10 GW Renewable Energy by 2030

Risk Factors (Ignore Mat Karo)

1. Crude Oil Price Volatility

Profit Direct Oil Price pe Dependent

2. Government Interference

PSU Hone ki Wajah se Pricing Control Possible

3. Renewable Energy Shift

Long Term me Fossil Fuel Demand Slow ho Sakta Hai

4. Declining Reserves

Past me Production Decline bhi Dekha Gaya

Technical Outlook

- Support Zone: ₹220 – ₹240

- Resistance: ₹260 – ₹275

- Breakout Above: ₹275 Strong Rally Possible

Trend: Sideways to Bullish (Medium Term)

ONGC Share Price Target 2030

| Year | Target |

| 2026 | ₹300 – ₹338 |

| 2027 | ₹359 – ₹375 |

| 2028 | ₹410 – ₹427 |

| 2029 | ₹459 – ₹492 |

| 2030 | ₹522 – ₹665 |

- Conservative Target 2030: ₹500+

- Bull Case Target 2030: ₹650+

Buy/Sell Strategy

Long Term Inveators:

- Buy on Dips ₹220 – ₹240 Range

- Hold for 3-5 Years

Swing Traders:

- Buy Near Support ₹235

- Target ₹260 – ₹275

Sell Kab Kare?

- Oil Prices Crash

- Govt Policy Negative

Expert & Analyst View

- Analysis Average Target: ₹288 (Short Term)

- Market View: Undervalued PSU Stock

- Recommendation: Hold/Accumulate

Pros and Cons

Pros:

- Strong Dividend Income

- Undervalued Stock

- Monopoly Type Position

- Oil Price Upside Benefit

Cons:

- Govt Control

- Slow Growth vs Private Companies

- Oil Dependency Risk

Overall Buy or Not?

Long Term ke Liye: Good Value Stock

Short Term: Volatile

Best For:

- Divedend Investors

- Value Investors

Not Ideal For:

- Fast Growth Seekers

Conclusion

ONGC ek Stable + Dividend Paying + Undervalued PSU Stock Hai.

Agar Aap:

- Patience Rakh Sakte ho

- Oil Cycle Samajhte ho

To 2030 tak Yeh 2x Potential Dikha Sakta Hai (₹500 – ₹650 Range)

FAQ (Frequently Asked Questions)

Q1. ONGC Long Term ke Liye Kaisa Hai?

Safe + Stable, But Slow Growth

Q2. Kya ONGC Multibagger Ban Sakta Hai?

Moderate Multibagger (2-3x Possible)

Q3. Dividend Milta Hai?

Haan, Strong Dividend Yield

Q4. Risk Kya Hai?

Oil Prices + Government Policies

Q5. 2030 Target Realistic Kya Hai?

₹500 – ₹650 (Market Conditions pe Depend Karega)

Disclaimer

Yeh Article Sirf Educational aur Informational Purpose ke Liye Likha Gaya Hai. Is Article me di Gayi Share Price Target, Analysis aur Opinions Author ki Personal Research aur Market Understanding Par Based Hain. Stock Market me Investment Market Risk ke Saath Aata Hai, Isliye Kisi Bhi Stock me Invest Karne se Pehle Apni Khud ki Research Karein ya Kisi SEBI Registered Financial Advisor se Salah Zarur Lein.

Is Article ka Purpose Kisi Bhi Stock ko Buy ya Sell Karne ki Recommendation Dena Nahi Hai. Author ya Publisher Kisi Bhi Financial Loss ke Liye Zimmedar Nahi Honge.

Mera naam Gopal Pramanik hai aur main ek Stock Market Enthusiast, Blogger aur Financial Content Creator hoon. Main Bharat Ka Share Bazaar.Com ka founder hoon, jahan par main logon ko Share Market, Investing aur Financial Awareness ke baare me simple aur practical knowledge provide karta hoon.